05 February 2020

By portermathewsblog

via domain.com.au

Get ahead of the curve by dipping your brush into 2020’s most coveted colours Photo: Annie Sloan

Get ahead of the curve by dipping your brush into 2020’s most coveted colours Photo: Annie Sloan

Looking to update your home? Fresh colour is an easy DIY and affordable way to up-style any home.

Get ahead of the curve by dipping your brush into the most coveted colours and steal these insider tips for the perfect painterly refresh, inside and out.

Lilac, pale pink and mint

Why: “With neutral colour schemes dominating the last few years, it’s time for some soft, subtle hues,” says designer Justine Brown from Chocolate Brown. “They complement neutrals and tie back with on-trend pale timbers, terrazzos and marbles beautifully.”

Where: A wash of mauve, rose, blush or mint adds colour and whimsy, and lives easily in any space as a neutral or pretty backdrop. “Introduce via your bed linen and soft furnishings,” says Brown. “Combine with tarnished brass or try a mint green laminate with pale timber and white cabinetry in the kitchen.”

We love: British Paints Lilac Lies, Dulux Mint Twist, Chalk Paint in Paloma.

Expert Tip: “These colours work harmoniously together,” says colour and paint expert Annie Sloan. “Add a stronger hue to prevent them looking too sweet, or white for contrast. For boldness, introduce yellow, black and white, or incorporate pastel floral fabrics for an English Countryside look.”

‘I love dirty mustard tones with pale timbers and concrete.’ Photo: Robert Walsh

Vibrant yellow and mustard

Why: “Yellow is so uplifting,” says Brown. “I love dirty mustard tones with pale timbers and concrete.”

Where: Yellow works anywhere and suits all furniture, artwork, and decor. It even works in kids’ bedrooms for a space they won’t outgrow. “It’s fabulous with tarnished brass bathroom fittings,” says Brown. “Or layer with blues, pinks and whites in the bedroom.”

We love: Dulux Dandelion Yellow, British Paints Yellow Mania, Porters Paints Amber.

Expert tip: “Mustard takes neutrals one step further in terms of depth,” says Brown. “It’s the perfect addition if your palette is looking bland.”

When the correct tones are applied, this is a palette that can be applied inside and out with ease. Photo: Felix Forest

Greige

Why: With grey on the wane, the combination of grey and beige provides fresh sophistication. “Greige evokes calm and stillness,” says designer Madeleine Blanchfield. “It’s subtle but gives the impression a space has been thoughtfully decorated. It’s warm without being overwhelming.”

Where: Greige looks beautiful with classic white trims or applied from top-to-bottom for real luxury. “It’s the perfect neutral and foil to add colour to,” says Sloan. “It works in most rooms and looks brilliant with reds, pinks and greens. It sits elegantly in the background, allowing colours to pop out from it.”

We love: Porters Paint in Grey Pepper, Chalk Paint in Country Grey

Expert Tip: “Taking photos of the beach and gardens allows us to pick colours within the greige spectrum,” says Blanchfield. “We use these natural tones to find a closer match in different paint ranges.”

A wash of mauve, rose, blush or mint adds colour and whimsy. Photo: Robert Walsh

Earthy tones

Why: Rich and moody, this palette provide an effortless connection between interiors and outdoors.

“Orange, red, tan and brown feel grounding,” says designer Nickolas Gurtler. “They feel good to live with because they are characteristic of nature which is always constant in our lives,”

Where: When the correct tones are applied, this is a palette that can be applied inside and out with ease.

“For opulence, choose dark unsaturated tones,” Gurtler says. “You can manipulate these colours to do almost anything.”

Expert Tip: Choose different shades and fine-tune the mood of your room. “Select one hue and use its multiple tones in different textures,” says Gurtler. “Be sparing or go bold. Both work.”

We love: Taubmans Barrel O Rum, Delta Clay

From grassy shades to desert hues, green delivers impact whilst feeling soothing to live with. Photo: Felix Forest

Back to nature green

From grassy shades to desert hues, green delivers impact while feeling soothing to live with.

Why: “Green is soothing and honest, or opulent and luxurious,” says Gurtler. “It depends on how it is used.”

Where: Apply everywhere, from walls and doors to pots and cabinetry. “I like green in the bedroom, bathroom and living spaces,” he says.

Expert Tip: High-gloss finishes provide luxury and impart a soft glow by bouncing light around a space.

“Combine deep hues with black, white and brass for opulence,” suggests Gurtler. “Unsaturated greens, like eucalyptus, pair well with greys, whites and blonde timbers.”

We love: Porters Paints Cosmos and Nori, Dulux Dinosaur

Comments (0)

30 May 2019

By portermathewsblog

via finance.nine.com.au

Australia’s housing market downturn is coming to an end, with leading economists predicting a spike in house prices as soon as July.

Property prices fell one per cent nationally in January, with CoreLogic data showing a smaller decline of 0.5 per cent in April – a result tipped to be repeated for May.

It comes after Commonwealth Bank’s incoming, home loan applications jumped to a 10-month high and strong predictions of interest rates cuts.

Expect to see a whole lot more of these in the coming months. (AAP)

Expect to see a whole lot more of these in the coming months. (AAP)

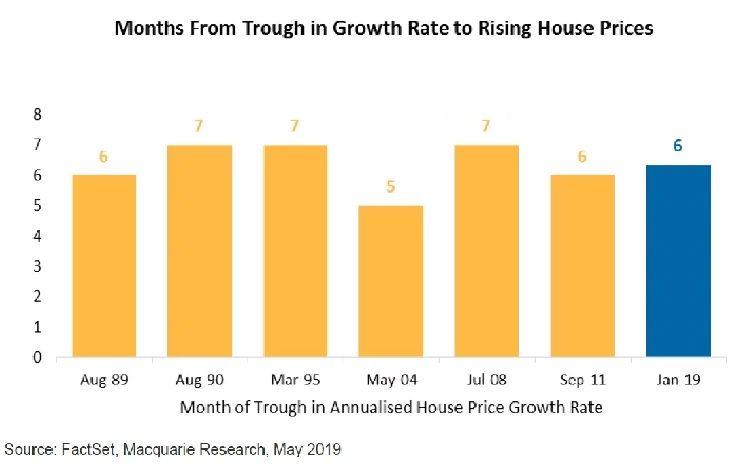

“Australia’s house price growth reached its worst on an annualised basis in January. Prices have continued to fall since then, but the rate of decline has slowed,” the bank wrote in a statement.

“If you look at prior cycles, an increase in house prices occurred five to seven months after the trough in the annualised growth rate. Using the average of six months, prices could rise by July.”

The bank said in every Australian house price cycle since 1989, price growth followed within seven months after the monthly annualised price decline bottomed.

Graph showing the trend repeating over the past 30 years. (Supplied)

Graph showing the trend repeating over the past 30 years. (Supplied)

Macquarie’s prediction extends further than past performance, with the bank also attributing looming interest rate cuts, relaxed lending conditions and the recent election result to its positive outlook.

“With the surprise Coalition election win, APRA’s policy change and an expected June RBA rate cut, we are more confident Australian house prices could rise within months,” the note read.

“This should flow through to better growth in housing finance and building approvals.”

AMP Capital chief economist Shane Oliver shares similar sentiments.

“The combination of the removal of the threat to property tax concessions, earlier interest rate cuts, financial help for first home buyers and APRA relaxing its 7 per cent interest rate test points to house prices bottoming earlier and higher than we have been expecting,” he said in a note.

“We now expect capital city average house prices to have a top to bottom fall of 12 per cent— of which they have already done 10 per cent — rather than 15 per cent and to bottom later this year.”

A swing in property prices has been supported with the Commonwealth Bank saying last week it saw the highest level of home loan applications in ten months.

This also coincides with CoreLogic data from the same period showing median home prices in Sydney and Melbourne increased by 0.3 per cent and 0.1 cent, respectively.

Prime Minister Scott Morrison’s victory has helped the market, economists say. (AAP)

Prime Minister Scott Morrison’s victory has helped the market, economists say. (AAP)

Nine finance editor Ross Greenwood said the threat of changes to the tax treatment on Australian housing created a lot of uncertainty in the market, but since Scott Morrison’s victory this has shifted to a “sense of immediate euphoria”.

“It is actually good news if people kind of feel OK about things,” he told Today.

“But the one thing about this is it now comes back to the old-fashioned leaders of the economy – what the Reserve Bank does, whether we get tax cuts.

“These are the things that put cold hard cash in people’s pockets. At the end of the day, that’s the thing that counts.”

Greenwood added tax cuts would have a bigger impact long-term on household budgets and finances than a decline in interest rates.

“The problem is because one-third of families have a mortgage, whereas two-thirds of families are trying to save for a mortgage to own their home and they have savings in the bank,” he said.

Comments (0)

22 November 2018

By portermathewsblog

Great news for the Western Australian economy, read the article below.

If we can be of help or offer advice on selling & leasing give us a call on 9475 9622!

By Josh Zimmerman Via: https://www.perthnow.com.au/business/housing-market/house-price-rise-on-cards-as-economy-confidence-improving-says-wa-premier-mark-mcgowan-ng-b881023908z

PREMIER Mark McGowan has this message for West Australians: buy a house now because the good times are coming back.

Exactly one year after The Sunday Times heralded early signs of life for WA’s stagnant economy, the results are in — and they are conclusive.

Data released on Friday showed the State’s domestic economy expanded 1.1 per cent in 2017-18, a remarkable turnaround after plummeting 7.1 per cent in 2016-17 and four consecutive years of decline.

This week another big step was taken towards WA reclaiming its AAA credit rating when Federal Parliament enshrined in law the hard-fought $4.7 billion GST reform package, which The Sunday Times has campaigned for since 2014.

Nearly every month this year has brought news of renewed activity in the mining sector. Rio Tinto, Fortescue Metals Group and BHP have all announced new workforce-hungry iron ore projects and the State now boasts seven lithium mines, with a second $1 billion lithium processing plant on the way near Bunbury.

Mr McGowan said he had not felt more confident about WA’s economic prospects since sweeping to power early last year.

“Every day you are seeing good signs,” he said. “The confidence is back in WA. You can feel it, you can see it and certainly it is an improvement on where it was.”

Mr McGowan tipped a turnaround in the long-declining property market and a jolt to stagnant wages would follow hot on the heels of renewed business investment.

Andrew Worland, the CEO of Rosslyn Hill Mining, and WA Premier Mark McGowan.Picture: Richard Hatherly

Andrew Worland, the CEO of Rosslyn Hill Mining, and WA Premier Mark McGowan.Picture: Richard Hatherly

“It is actually a good time to buy (a house),” he said.

“I would encourage people. Prices are low yet economic activity is picking up and so that will inevitably be followed by (demand for) housing.”

The Sunday Times joined Mr McGowan in Wiluna on Thursday to visit the oft-maligned Paroo Station lead mine, where a $US150 million investment in world-first processing technology is set to bring the operation back to viability while eliminating environmental issues previously associated with transporting lead concentrate.

The Rosslyn Hill Mining venture has just received environmental approvals to expand and build an advanced hydrometallurgical facility, which will convert lead concentrate to bars without the traditional smelting process.

Lead is among the suite of minerals abundant in WA that Mr McGowan hopes will catapult the State into global leadership in the renewable energy sector.

To that end, his Government has set aside $5.5 million for a future battery research centre, but recognises that WA-made batteries are a long way off. “That would be a longer-term initiative,” Mr McGowan said.

Comments (0)

15 October 2018

By portermathewsblog

via reiwa.com.au

Affordability in Perth’s residential sales market improved during the September 2018 quarter, with house and unit prices softening marginally.

Affordability in Perth’s residential sales market improved during the September 2018 quarter, with house and unit prices softening marginally.

REIWA President Damian Collins said there was excellent opportunity for buyers and investors to take advantage of current market conditions to secure their next home or investment property.

“While the worst of the market downturn appears to be behind us, the results of the September 2018 quarter reveal conditions are favourable for buyers and investors,” Mr Collins said.

Median house and unit price

reiwa.com data shows Perth’s median house price should settle at $505,000 for the September 2018 quarter.

“This is 1.9 per cent lower than the June 2018 quarter median and one per cent lower than last year’s September quarter,” Mr Collins said.

“While quarterly median figures can be more subject to stock composition changes, the fact that the annual change is only one per cent lower suggests that we are at or near the bottom.

“It was a similar story for the unit market, with the median expected to settle at $395,000, which is 1.3 per cent lower than the June 2018 quarter and 2.5 per cent lower than the September 2017 quarter.”

While the overall market experienced a decline in median house price during the quarter, 57 suburbs across the area bucked this trend.

“The top performing suburbs for median house price growth were Swan View, East Cannington, Como, Hillarys and Cottesloe.” Mr Collins said.

“In the unit market, Maylands, Midland, Tuart Hill, Fremantle and Claremont were the suburbs with the strongest price growth.”

Sales activity

There were fewer sales in the September 2018 quarter than there were during the June 2018 quarter.

Mr Collins said reiwa.com data showed 6,428 sales for the quarter, which was 4.9 per cent lower than last quarter.

“It’s not uncommon to experience a decline in sales during the September quarter, with West Australians typically less inclined to search for property during winter. We tend to see activity slow during the winter months before increasing again as the weather warms up,” Mr Collins said.

The share of house sales in Perth has increased, with reiwa.com data showing houses now comprise 74 per cent of all sales, compared to 65 per cent at the same time last year.

Perth’s top selling suburbs for house sales during the September 2018 quarter were Baldivis, Canning Vale, Morley, Dianella and Gosnells, while the suburbs to record the biggest improvement in house sales activity were Cooloongup, The Vines, Alexander Heights, Mirrabooka and Wattle Grove.

“It’s a good time to buy, which is reflected in the fact a higher proportion of houses are now being sold. This shift in the composition of sales (houses, units and land) indicates buyers are more inclined to purchase a house than they might have otherwise been. This can be attributed to housing affordability improving across the metro area, which has made buying a house a more attainable property purchase,” Mr Collins said.

“We’ve also seen an increase in activity between the $350,000 and $500,000 price range during the September quarter, which is pleasing as it indicates first home buyers remain an active component of the Perth market.”

Listings for sale

There were 13,850 properties for sale in Perth at the end of the September 2018 quarter.

Mr Collins said stock levels across the metro area had declined 3.7 per cent during the quarter.

“It’s pleasing that, although there were fewer sales this quarter, listing stock continues to be absorbed.

“This is the third consecutive quarter we’ve seen listings for sale decline, which is a positive step forward in the market’s recovery,” Mr Collins said.

Comments (0)

01 October 2018

By portermathewsblog

via reiwa.com.au

Author: REIWA President Hayden Groves

Real estate transactions are complex. For many West Australians, it can be a challenge to determine their individual rights and responsibilities when it comes to dealing with property issues.

Real estate transactions are complex. For many West Australians, it can be a challenge to determine their individual rights and responsibilities when it comes to dealing with property issues.

REIWA launched a public information service in 1992 to assist buyers, sellers, tenants and landlords navigate their property journeys. This valuable service allows members of the WA public dealing with a REIWA agent to find answers to their real estate queries and concerns.

Last financial year more than 20,000 phone calls were placed to the REIWA Information Service (2,000 more than the previous financial year), with West Australians seeking clarification and assistance from the Institute on a wide range of real estate matters.

As the WA market has slowed these past few years, the REIWA Information Service has seen call volumes increase. Residential property management continues to be the most common topic the public ring about, with 70 per cent of all phone calls for the year to date received from tenants and landlords. The remaining 30 per cent of calls have generally related to residential sales.

When it comes to WA tenants, they most commonly call REIWA to discuss the early termination of their rental lease. They also want to know what rights their landlords have to enter their property while tenanted and what rights they have with regards to repairs and maintenance.

Landlords, on the other hand, most commonly call to seek information on a tenant’s obligation to pay rent, to find out how the court system works in order to claim damages and to clarify their rights around abandoned goods.

In the residential sales market, buyers who call the REIWA Information Service generally do so to get information about their obligation to obtain finance approval within a period of time. They also commonly call to clarify their rights for the pre-settlement inspection. While WA sellers most frequently ring to find out about the settlement process, satisfying contractual conditions and to discuss buyer requests which are not addressed in the contract for sale.

The REIWA Information Service team is comprised of two full time staff members and 70 local REIWA agents who give three hours of their time every few months on a voluntary basis.

When you call up, you are given direct access to these local property experts who can educate you on areas you’re unsure about and help resolve any tricky property matters you might be facing.

If you are dealing with a REIWA agent and have a real estate query you want answered, I’d highly recommend contacting the REIWA Information Service on 9380 8200 for assistance.

Comments (0)

25 September 2018

By portermathewsblog

therealestateconversation.com.au

Over the past six months, grey clouds have been building in the distance for borrowers, and for many, the brewing storm is yet to hit in full force.

Australia’s current lending landscape is a tough one. Moves by legislators and regulators to kerb borrower enthusiasm have created headaches for those now looking to build a

portfolio.

That said, there is opportunity ahead for those able to weather the challenge.

The state of play

The runaway nature of Australian property prices in Sydney and Melbourne from 2012 was causing concern for legislators.

It was claimed investors were taking up all the stock and isolating first homebuyers from the market – and there were no indications things were going to slow down.

In 2014 the Australian Prudential Regulation Authority (APRA) responded by instructing banks to cap growth in investor lending to 10 per cent of their total loan book.

An additional move in 2017 by APRA required banks to keep interest-only loans to less than 30 per cent of their mortgage portfolio too.

While both these measures were said to be temporary – in fact, the first has been recently relaxed – they appear to have done their job too well with investor-loan growth now at single-digit percentages.

Add to the mix the current banking enquiry. It’s findings so far have levelled criticism at bank practices.

To compensate and prepare for the eventual recommendations, lenders are already tightening their requirements from borrowers – particularly investors.

What’s happened

The upshot is that getting a property loan approval at the moment is tough.

It’s been a fast turnaround too. Whereas six months ago a bank customer might have been approved to borrow $800,000, nowadays that same client might be lucky to get $500,000.

That means many who contract to purchase based on a pre-approval gained under the old guidelines, will find their application knocked back under the bank’s new rules.

Another reason for impending mortgage stress is many loans are about to roll over from Interest-only to Principal-and-Interest in the next 12 months.

This means higher repayments for some already stressed borrowers.

These customers will have little choice but to accept the new loan terms being offered by their current lender, because competition for interest only lending will be virtually non-existent.

Here’s the perfect storm scenario:

- The cost of money will go up,

- The availability of money will drop,

- And, in certain markets, value growth will be non-existent for a number of years.

Is there opportunity?

In short – yes, but it’ll be those who got their affairs in order early who’ll benefit most.

Investors who’ve built a resilient portfolio are certain to take advantage.

Your investment strategies must be long-term so you can smooth out the peaks and troughs of market and finance cycles in order to secure your future for decades to come.

1. Have impeccable records

Now more than ever, it’s important to have kept your financial records in tip-top order.

By this, I mean you need to know your numbers inside and out, and back to front.

It all has to be documented as well. Not so long ago, for example, it was acceptable to front up to the bank with little more than your estimated living costs and gross income, and with a signed statutory declaration as back up.

Nowadays, it’s a case of being able to account for every dollar. You may have put “Annual clothing allowance – $1000” in the loan application, but today’s banking credit departments are checking your credit card statements as well.

They know your Gucci shoes and Burberry briefcase cost twice that, and they’re willing to say, “No!”

Having impeccable records means you can accurately account for every dollar.

It also demonstrates to the bank that you can stay on top of your loan commitments.

Being a good customer really can pay dividends in these trying times.

2. Maintain cash flow

Cash flow is king when it comes to loan serviceability, so if you’ve built a multi-property portfolio, make sure your income isn’t overextended.

Key to this is portfolio diversification. We always recommend maintaining a buffer as part of your investment strategy because changes in interest rates, personal circumstances and the cost of living are inevitable.

In addition, banks are now upping their ‘stress test’ on client’s finances – increasing their own interest rate and cost tolerances on your supplied numbers.

Being on top of your cash flow can be the difference between a yes or no on your next loan.

3. Equity buffer

Along with cash flow you must maintain an equity buffer as well.

Having adequate equity is essential to a lender’s requirements.

The problem that often occurs during a period of high property value growth (like recently) is some owners use their new-found equity on unproductive debt.

They might spend up big on their credit cards and then consolidate that debt into their house loan.

While they’re at it, they might get a bit extra from the bank in order to buy a new car or go on holiday.

These borrowers are not allowing for the future and have effectively re-bought their property off the bank at today’s prices because they ‘feel wealthy’.

The best opportunities are there for those who have liquidity in their equity.

I’m a big believer in making your money work for you and if your equity isn’t liquid, you can’t capitalise on opportunities when they arise.

Building a resilient portfolio in times of great growth is essential so you not only survive any eventual slowdown, but can pounce on newly revealed profitable prospects.

If you’ve failed to prepare for our new, tougher financial times, now might be the chance to catch your breath, talk to an expert strategist and plan for the cycles next turn.

After all, the state of your wallet dictates the state of your mind.

Comments (0)

17 September 2018

By portermathewsblog

via therealestateconversation.com.au

The property industry is continuing to drive the Australian economy according to the latest economic growth data.

The Australian economy grew by 0.9 per cent in seasonally adjusted terms in the June 2018 quarter National Accounts released last week, with annual growth of 3.4 per cent.

Investment in new dwellings increased 3.6 per cent for the quarter, with strong results in Victoria and South Australia.

The construction industry grew by 1.9 per cent for the quarter.

Construction within the residential property sector grew by 3.1 per cent and non-residential property sector by 1.3 per cent over the quarter.

The ABS noted that the recent pickup in new dwelling investment reflected strong approvals in early 2018 which are now flowing through to commencements.

“The property industry is helping to propel economic growth to its highest level since 2012, highlighting its importance as a driver of jobs and economic prosperity,” said Ken Morrison, Chief Executive of the Property Council.

“Our national economic well-being depends on a strong property industry, supported by smart investment in vital public infrastructure for our growing cities.”

“The benefits of growth are overwhelmingly positive, but must be locked in and supported by good planning and smart infrastructure investment to ensure all Australians reap the gains,” Mr Morrison said.

Comments (0)

10 September 2018

By portermathewsblog

via therealestateconversation.com.au

Malcolm Gunning, President of the Real Estate Institute of Australia (REIA), and Leonard Teplin, Director of Marshall White debate the potential implications the most recent leadership spill could have for the residential property market.

It feels like we’ve had more leadership spills than seasons of The Bachelor, and some industry leaders are worried that Australia’s reputation for changing Prime Ministers at the drop of a hat is having negative consequences across the property market.

Director of Marshall White, Leonard Teplin says the constant change of leadership in Australia is driving residential buyer sentiment to an all-time low, and it’s the Australian public who are left to sit back and watch the fallout, again and again.

“There are no real winners, only losers. The Australian public must once again sit and watch while the effects ripple across our economy and property market,” Mr Teplin said.

“It’s no secret that every time there is an election, market sentiment drops, people delay purchases and put off big decisions until the new leader has been decided, and election promises turn into policies.

“In real estate, this sentiment is reflected in weaker conditions as buyers cautiously await the inevitable policy changes and market overcorrections that are sure to follow suit.

Industry leaders are concerned about the potential implications the leadership spill could have on the property market. Image by Adz via WikiCommons

Industry leaders are concerned about the potential implications the leadership spill could have on the property market. Image by Adz via WikiCommons

“As Scott Morrison gets set to take over as the nation’s leader, property purchasers both locally and abroad will be questioning what this change in direction will mean for them and their investments,” Mr Teplin told WILLIAMS MEDIA.

But Malcolm Gunning, President of the Real Estate Institute of Australia (REIA) doesn’t believe the leadership spill will have a drastic impact on the property market.

“I don’t think there will be any change because Scott Morrison was really the architect of the current economic policy,” Mr Gunning told WILLIAMS MEDIA.

“Tougher lending criteria introduced by the APRA, and the banking royal commission is what’s really having the biggest influence on the market at the moment.”

Jock Kreitals, CEO of the REIA agrees.

“In terms of the recent changes of Prime Ministers and Ministers, I do not see any impact on the market attributable to this. The policy of the Coalition regarding negative gearing and CGT remains unchanged.

“The PM as the previous Treasurer has reiterated the position a number of times. Further, the PM well understands the impact of changes in policy having worked in a policy role in the property sector,” Mr Kreitals told WILLIAMS MEDIA.

Real Estate Institute of New South Wales (REINSW) CEO, Tim McKibbin says the new Prime Minister should put good fiscal policy ahead of economically damaging, populist politics.

“Those advocating for removing the deductibility of expenses incurred in earning assessable income in the residential property market are damaging people’s ability to acquire a home,” Mr McKibbin told WILLIAMS MEDIA.

“This is adversely impacting the property industry – Australia’s biggest employer – and playing petty politics in the misguided belief it will promote their personal brand.”

Potential implications for foreign investment revenue

Mr Teplin believes the latest leadership spill could impact international investment revenue.

“A stable government is a pillar of optimised liveability and one of the main reasons Australia has enjoyed a consistent influx of foreign investment into the real estate market, in turn driving the delivery of new infrastructure and economic progress,” Mr Teplin said.

This recent setback could be detrimental for Australia’s international investment revenue, “which serves a much-needed portion of the market that drives new residential supply and delivers stock to the rental market,” Mr Teplin continued.

Mr Gunning told WILLIAMS MEDIA the message the government is sending to overseas investors is what worries him the most.

“Our government seems to be very stable – and I’m not talking about leadership changes – but both parties are reasonably well aligned in policy. What sends the discouraging message is the tightened immigration and the taxing of foreign investors,” Mr Gunning said.

“Chinese investment into Australia’s residential property market has stopped, and I can say with conviction that the message this sends back to China is that they’re not welcome. So it’s more about the message it sends by the government rather than the changes in leadership.”

“It will take investors out of the market”

If Labor were to win the next election, as it appears they will, Mr Gunning says the rental market will suffer.

“Labor is absolutely rusted on to negative gearing. They are of the opinion that it will help affordability, which is completely incorrect. What it will do is drive up rents because there will be fewer people buying investment property,” Mr Gunning said.

“There has been 13 per cent growth in rent over the last five years, which is historically low and below inflation. If Labor gets in, it will take investors out of the market which will hinder supply – up goes the demand and the cost of rent.”

Mr Kreitals told WILLIAMS MEDIA that if Labor were to be elected, the current market falls would be “exacerbated”.

“Labor has on many occasions, including recently, reiterated the position that it took to the 2016 election to change negative gearing and CGT arrangements. In the lead up to the 2016 election, a number of studies were undertaken to examine the impact of such changes. In short, housing prices will fall and rents will go up.

“SQM Research, for example, forecast that in the first year of the policy, prices would fall by up to 3 per cent, and by up to 8 per cent and 4 per cent in the following two years.

“It needs to be remembered that at the time of the 2016 election, property prices were rising. Introduction of Labor’s measures would exacerbate the current market falls and flow on to the construction industry and economic growth,” Mr Kreitals said.

Industry leaders debate the implications the leadership spill could have on the property market. Image by Maxmillian Conacher via Unsplash.

Industry leaders debate the implications the leadership spill could have on the property market. Image by Maxmillian Conacher via Unsplash.

And if stability is the cornerstone of sound investment, Mr Teplin says buyers will look to take their money elsewhere for more predictable returns in safer markets.

“As sentiment plummets and the population continues to grow faster than new stock can be delivered to meet the market, now more than ever we need a strong, stable, united government to help rebuild the real estate market and deliver stock to where it is most needed,” Mr Teplin said.

“Political in-fighting isn’t just bad for business on a global scale – its effects are felt right across the property market long after party room vengeance has been executed.”

Affordability improving for renters, first home buyers

The June quarter 2018 edition of the Adelaide Bank/REIA Housing Affordability Report found that affordability has improved for renters and the number of first home buyers increased during the second quarter of 2018.

The number of first home buyers increased to 28,401 – an increase of 7.3 per cent during the quarter and an increase of 20.6 per cent in the June quarter of 2017.

First home buyers now make up 17.8 per cent of the owner-occupier market, compared with 14.3 per cent at this time last year.

Rental affordability improved in New South Wales, Victoria, Queensland, South Australia and Tasmania, remained steady in Western Australia and declined in the Northern Territory and the Australian Capital Territory.

New South Wales remains the least affordable state for renters, where the proportion of income required to meet rent repayments is 28.8 per cent – 4.7 percentage points higher than the national level.

Scott Morrison admitted last year that Australia has a housing affordability problem and announced a number of measures in the May budget.

“There are no silver bullets to make housing more affordable. But by adopting a comprehensive approach, by working together, by understanding the spectrum of housing needs, we can make a difference,” Mr Morrison said at the time.

Mr Kreitals told WILLIAMS MEDIA it’s worth considering the importance of property to the economy, highlighted by the latest GDP figures.

“For the quarter, the economy grew by 0.9 per cent and 3.4 per cent for the year, which is the fastest rate of growth since the September quarter 2012.

“The property industry is continuing to drive the Australian economy with investment in new dwellings increasing 3.6 per cent for the quarter. The construction industry grew by 1.9 per cent for the quarter and 5.5 per cent over the year,” Mr Kreitals said.

Comments (0)

20 August 2018

By portermathewsblog

via www.therealestateconversation.com.au

Reaching the 25 million population milestone should be the catalyst for the creation of productive, vibrant and liveable cities that will underpin Australia’s future prosperity.

Source: Reiwa

Source: Reiwa

Australia’s future rests overwhelmingly with our cities and their ability to become high amenity, high liveability engines of our economy,” said Ken Morrison, Chief Executive of the Property Council of Australia.

“Our population is growing strongly and most of that growth is occurring in our cities. We need to redouble our focus on policies that support investment, planning and collaboration to create the great Australian cities of the future.

“Population targets, decentralisation policies or adjusting immigration rates can’t allow us to take our eyes off the main game which must be our ability to create great cities for current and future generations of Australians.

“The growth of our cities is part of an international trend for cities to be a magnet for people, business, investment and economic and cultural activity.

“We’re not alone in needing to plan, invest and manage for change as the worldwide trends towards urbanisation gathers pace in this ‘metropolitan century’,” Mr Morrison said.

The drivers of urban growth were set out in the ‘Creating Great Australian Cities’ research published by the Property Council earlier this year.

It highlighted the growing economic importance of cities around the world, and set out a series of principles and recommendations based on the experience of other fast growing cities of similar size to Australia’s. These cities are capturing an expanding share of business, immigration, visitors, talent and capital flow.

The report found that Australian cities had strengths, including their economic performance investment attraction, higher education and natural environment but they were performing poorly in several key areas critical to success in the metropolitan century, including issues such as transport congestion, fragmented systems of governance, infrastructure investment and limited institutions at a metropolitan scale to manage growth.

“Our cities are at the heart of Australia’s economic, social and cultural life, attracting people, investment and services that drive innovation, creativity and enterprise,” Mr Morrison said.

“Any population policy that doesn’t strengthen Australia’s ability to create great cities of the future is completely missing the mark.

“Our cities are already a great competitive advantage for Australia, bringing together the people, services and infrastructure to drive our economic competitiveness.

“We need to keep investing in the right infrastructure, plan for a growing future and put in place smarter systems of metropolitan governance to capture the full potential of the metropolitan century while sustaining the quality of life and access to services that Australians value.

“We need to take on both the challenges and opportunities of the ‘metropolitan century’ and not run away from the reality that growing cities can be successful cities and great places for people to live and work.

“With the right planning, policies and ambition, we can create truly great cities for a growing Australia,” Mr Morrison said.

Comments (0)

13 August 2018

By portermathewsblog

via therealestateconversation.com.au

As we head into 2018, I believe this year will be one of market transition across the country.

It will also be a year of finance, with those who can secure it likely to be the ultimate winners. It’s no great surprise that Sydney and Melbourne are transitioning out of the strong price growth they’ve experienced over recent years.

However, that doesn’t necessarily mean they’re going backwards. Instead, their growth may fall back to one or two per cent annually. That market transition will be driven by reduced consumer confidence, which is a reflection of the price of money as well as how easy it is to secure finance. Confidence also usually wanes when the media starts speculating about softer market conditions.

It’s clear that Sydney’s market has already come off the boil and Melbourne’s is likely to follow suit but in a more moderate way.

Positive transition

It’s important to realise that transitions happen in both directions, with some markets slowing while others are strengthening. I believe this will certainly be the case for Brisbane, which is on track to transition to stronger market conditions.

That said, Brisbane is a city of different markets with the inner-city in the midst of it’s well-publicised new unit oversupply. It is Brisbane’s outer suburbs that represent good value and cash flow, as well as attractive lifestyle drivers, that will experience the most improvement in my opinion.

Of course, there are already increasing numbers of interstate migrants into Queensland given it’s housing affordability as well as it’s many attractive lifestyle opportunities.

SA and WA back in the game

I also believe it will be a year of positive transition for South Australia and Western Australia. South Australia always seems to lag behind other capital cities and by the time most investors realise what’s happening it’s too late. The truth is that South Australia’s transition is already happening.

In Adelaide, however, it’s only the 15-minute ring around the CBD as well as areas like Christies Beach that are worth considering. We all know WA has been woeful over recent years, but this could be the year it finally turns a corner. The State Government has been concentrating on jobs growth, with employment numbers reportedly starting to improve. If locals start spending money because they’re more confident about their livelihoods, then, that in turn will stimulate the market.

However, when I say WA, I mean Perth and select areas within the city as well. If interest rates increase, even if only by a blip, those green shoots of confidence might evaporate as fast as they appeared. Tasmania will continue to percolate until cash flow doesn’t look as attractive as other areas, such as Brisbane. I remain skeptical about Tasmania’s growth because it’s mainly being driven by investors chasing investors purely because of affordability.

Owner-occupiers aren’t the ones who are pushing up prices.

I believe it may lurch from under-supply to over-supply pretty quickly – and then you’ll probably have 10 years of no price growth at all.

A question of money

We’re now into our third calendar year of lending restrictions and I don’t believe they’re going anywhere anytime soon. Investor numbers have only recently started to slow so there will need to be more evidence before APRA loosens it’s grip on investment lending. Banks might want more flexibility but it’s unlikely to happen. So 2018 will be a year of market transition but it will also be a year of finance. The price of money remains cheap but it’s availability continues to be constrained.

That’s why I believe it will be the sophisticated investors who know which markets are transitioning to the positive – and who can secure finance – who will be the property victors by the end of the year.

Comments (0)

30 July 2018

By portermathewsblog

via The West Australian

The West Australian economy is “out of the woods”, one of the nation’s most respected forecasters has declared, with housing and wages finally gaining traction.

Amid warnings the Turnbull Government was making the same mistake of the Howard government by spending a temporary revenue bump on expensive personal income tax cuts, Deloitte Access Economics said the outlook for WA was definitely brightening.

The State endured its worst year on record through 2016-17 while the domestic economy had been in the doldrums for the past four years. But a string of data, including job figures, point to an important turnaround.

Deloitte Access director Chris Richardson said it was now clear WA was recovering from the economic “wave” that was the end of the mining boom.

He expects a lift in retail sales, population growth, wages and housing construction will all improve through this year and accelerate into 2019-20.

Wage growth alone is tipped to more than double the insipid 0.6 per cent growth endured by private sector workers last financial year. “WA’s economy is out of the woods, but it isn’t quite yet out of the doldrums,” Mr Richardson said.

“The good news is that WA’s economy is gradually making its way on to a more settled and sustainable path. The State is restructuring and rebalancing and looking for non-mining related sources of growth.”

While most focus has been on the collapse in engineering spending by the mining sector, Deloitte Access highlighted the step-up by the State Government to fill the void.

It said the first stage of the $3 billion Perth Metronet, which includes 72km of rail line and 18 stations, would give a needed boost to the local economy. The situation is a little different for the Federal Budget, with Deloitte Access concerned that recent tax cuts are built on a mirage of improved tax revenues.

Mr Richardson said tax cuts were built on an increase in tax revenues that was likely to be transitory. The Budget was also expecting to absorb the cuts while it was still in deficit.

He said a gradual slowdown in China would eat into the better tax collections from the resources sector while a tightening of credit would hit east coast property markets. “Oz has repeated an old mistake: spending a temporary revenue boom on permanent promises,” he said.

Comments (0)

20 July 2018

By portermathewsblog

via houzz.com.au

Passionate about technology? A home-automation system is likely to be on your wish list – here’s what you need to know

In this practical series, we ask experts to answer your burning home and design questions. A premium home-automation system – also known as a smart-home system – allows you to control multiple functions in the home, such as lighting, heating and cooling, audio, security, door locks and even kitchen appliances – from a single device, be it a touch-screen remote control or an app on your phone or tablet, from wherever you are in the world.

Tempted? Here, Trevor Rooney, director of residential markets at Crestron, reveals everything you need to know about setting up a home-automation system in your own abode.

Home automation is all about convenience. Having the ability to control core elements in your home remotely, such as lighting, heating, entertainment and front-door access, can save time and make life run more smoothly.

Image: Crestron

What sort of things can a home-automation system do?

- Give you remote access to door locks so you can control who has access to your home when you’re not there.

- Switch lights on and off remotely or connect them to a timer or sensors, so they go on automatically (also great for security when you’re not home).

- Control heating or cooling so you can come home to a warm interior in winter or a cool one in summer.

- Give you remote access to alarms and surveillance systems; you will be notified if anyone approaches your home and can see who is at your front door. You can also switch surveillance on and off remotely.

- Change the television channel or switch the set on or off via voice command.

- Set your coffee machine to turn on automatically in the morning (it will even brew you a cup before you get out of bed).

- Automate your pool and pond cleaning, with the ability to adjust settings from your smart device while you’re not at home.

For even greater convenience, you can pre-determine the settings on your automated system for lighting, heating and entertainment to suit different situations. For example, you could set the system to control various elements simultaneously, so that when you go to bed it turns off all the inside lights, switches on the security camera at the front door, adjusts the kids’ night lights, and switches off the heater – all with one swipe of your smart-screen remote or an app on your phone.

Can automation cut my energy bills?

Absolutely. Here’s how:

- Accidentally left your lights on when you left the house? With home automation, you can switch lights off from wherever you are.

- Connecting blinds to a sensor-controlled system means they’ll close automatically when the temperature reaches a certain point, keeping your home cooler and reducing air-conditioning costs. You can also keep your home naturally cooler by setting up an automated shading system for overhead or exterior window shades.

- No more overheating your home unnecessarily; by installing a smart thermostat, your heating will switch off automatically when the temperature reaches a certain level.

How is a home-automation system different to a smart-home assistant?

Devices such as Google Home and Amazon Echo are great for convenience. They can perform simple tasks by using voice recognition, such as checking the weather, reading out the day’s headlines or performing Google searches.

A premium home-automation system is far more sophisticated. It allows you to automate several different devices through one simple-to-use interface or an app on your phone. So, instead of having five different remote controls to manage your various devices, you just have the one platform, which can be controlled by voice or touch.

Image: Crestron

Image: Crestron

How does voice control work?

Systems such as those at Crestron can be connected to Amazon Echo’s Alexa Voice Service to enable voice control. This allows you to give voice commands, such as ‘Alexa, turn off the kitchen lights’ or ‘Alexa, raise the temperature in the family room by five degrees.’

You can also control multiple systems simultaneously through a number of preset scenes. For example, in the morning you could say ‘Alexa, tell Crestron to activate Morning Theme,’ and the blinds will slowly open, the lights will switch on and a warm shower will start running in the bathroom. Or, if you want to set the mood for an intimate dinner party, simply say, ‘Alexa, tell Crestron to activate Intimate Dinner.’ The dining room lights will dim, the window coverings will adjust and soothing music will play from your speakers.

What should I expect to pay?

This depends on the level of automation you want. Crestron’s new PYNG 2.0 platform (available later this year), which controls audio/visual functions, such as the television, Foxtel, Apple TV and Sonos, starts from around $3,500. This would include the processor and a touch-screen remote control. Incorporating lighting and shading solutions into a home-automation system would see this cost rise to around $10,000, depending on the size of the space.

A fully connected smart-home system starts from around $25,000, depending on the size of the property.

Can I retrofit an automated system?

It’s best incorporated during the building phase. However, it’s certainly possible to install after the build.

Comments (0)

16 July 2018

By portermathewsblog

via therealestateconversation.com.au

Be a smart investor and have a loan strategy.

You have saved away and have enough cash to consider purchasing property as an investment. Like any purchase, it is a huge one so having a strategy in place will keep you focused and ensure that you are doing as much due diligence as you can for a successful investment.

Not many successful investors became successful by accident – we recommend you start by seeking professional financial advice to really determine what your borrowing capacity is and how realistic your investment is.

Debt does not have to be scary, unless it is the wrong type of debt. In an ideal situation, you will want your debt to be productive and if you have planned how your cash flow will be affected, then you can have a clear understanding of how purchasing that next investment will affect your lifestyle. Productive debt in our eyes can be used as an advantage to buy an asset or generate income such as rental income.

Understanding your loan strategy

If you are looking to invest in multiple properties, we think it’s important to understand the short and long term perspective of property ownership. You have to think about how this next loan or investment is going to influence your life and your cash flow as well as what the situation might look like with your third or fourth investment. We say this as it can really make a difference in the type of property you purchase in the first place.

Think about how positively or negatively geared loans will affect what you purchase or how you live in the future. It may seem odd to be thinking so far in advance, but we think it is important to really understand your financial situation and also the results you would like to achieve as a property investor.

This is where we think it is important to be surround by the right advice. The right financial advisor for you will be able to help you plan the various scenarios to suit your end goal – after all everyone has different goals in their lives.

Comments (0)

12 July 2018

By portermathewsblog

via domain.com.au

With Australia’s major supermarkets banning the plastic bag it’s a good time to get on board #PlasticFreeJuly.

The initiative, whereby people pledge to reduce plastic from their lives for a month, is a great opportunity to learn about plastic-free eco alternatives beyond the tote bag.

Founder of the Plastic Free July Foundation, Rebecca Prince-Ruiz, says while plastic is an extremely useful material the fact it’s designed to last forever causes problems for the environment.

One of the biggest impacts is, of course, on wildlife. But plastic is a huge problem for humans too. Plastic bags contain a cocktail of chemicals that leach into the environment and increase up the food chain. “The UN Environment said it’s one of the greatest environmental challenges of our time,” Prince-Ruiz says.

Images of the Great Pacific Garbage Patch might suggest it’s a problem happening elsewhere. “CSIRO research found plastic in every beach in Australia,” Prince-Ruiz says. “And because we have high concentrations of wildlife, we’re the area in the world where seabirds are most at risk.”

Only 9 per cent of all plastic we’ve made on our planet is recycled, according to Prince-Ruiz. “This is a problem we can’t recycle our way out of. We need to rethink our use of this material.”

She suggests eliminating all single-use throwaway plastic such as plastic lollypop sticks, bottle caps, drink bottles and bags. “These are what we’re finding in our environment. It’s not about being perfect, or a competition. It’s about saying ‘hey, I’m going to try’.”

Frustration with sourcing plastic-free products led Sydney-based Lottie Dalziel to found an online marketplace where consumers can purchase plastic-free products all in one place. Launched in March, banish offers more than 460 products across 22 eco-friendly and cruelty-free brands, and is part of a growing movement to rein in the problem of plastic waste.

From the quirky and old-fashioned, to the funky and plain brilliant, here’s a glance at what’s out there to help you replace plastic in the home in July and beyond.

Kitchen

Beeswax wraps

Use to replace cling wrap. “It comes in funky colours and is a piece of fabric coated in beeswax,” Dalziel says. “Using the heat in your hand, it moulds. You just unwrap and rinse in cold water and use again.”

Beeswax wraps can replace cling wrap. Photo: Beeutiful.com.au

Beeswax wraps can replace cling wrap. Photo: Beeutiful.com.au

Lunch skins

The lightweight fabric bags come with a velcro closure and replace plastic lunch and snack bags.

Reusable produce bags

“Take these shopping with you and put your fresh produce into them, Dalziel says. “Keep them in their bags and it helps separate them in your crisper.”

Knitted and fabric cleaning cloths

Washable and re-usable, these replace your Wettex or Chux.

Coconut fibre scourers

A trendy accompaniment to your au naturel wooden chopping board.

Reusable straws

Choose from bamboo or stainless steel options.

Reusable bamboo straws. Photo: Banish.com.au

Reusable bamboo straws. Photo: Banish.com.au

Tea strainers

Combine the old-fashioned metal tea strainer with loose-leaf teas to banish plastic from your morning cuppa.

Bamboo takeaway cutlery

Chuck these in your lunchbox or buy in bulk for parties instead of the plastic variety.

Dishwashing tablets

Add a tablet to your dishwasher compartment and use as normal. Lil Bit sells a Cajeput-scented, Himalayan salt tablet.

Dust brush

Eco-Max offer a handmade and biodegradable recycled timber and coconut fibre dust brush.

Himalayan salt dishwashing tablets. Photo: Lil’ Bit

Himalayan salt dishwashing tablets. Photo: Lil’ Bit

Bathroom & personal hygiene

Shampoo and conditioner bars

Handmade, full of yummy ingredients and sure to start a trend. Get them at Lush and Beauty and the Bees.

Deodorant paste

Scent up with this option from Good & Clean. A portion of profits goes to your conservation project of choice.

Bamboo toothbrushes

“Cut off the bristles and the bamboo is completely biodegradable,” Dalziel says.

Dental lace

Made from Mulberry silk and mint-flavoured, it comes in it’s own refillable glass and stainless steel container. Get it at Ecostainable.

Metal razors

Built to last, you probably have one in your cabinet. For something new and nifty try the Parker Safety Razor.

100% natural deodorant paste. Photo: Good & Clean

100% natural deodorant paste. Photo: Good & Clean

Menstrual cups

Made with soft, medical-grade silicon, menstrual cups are used like tampons. Find them at Banish and other stockists.

Biodegradable cotton buds

Go Bamboo sell biodegradable bamboo cotton buds.

Tooth and gum powder

Natural ingredients mean this is also better for you. Buy it online at Banish.

Laundry

Soap nuts/soap berries

The saponin-rich shells of the Sapindus Mukorossi tree nut produce foam when mixed with water. “Add about seven nuts to your washing load in a bag,” Dalziel says. (Micro-plastics in traditional detergents end up in the world’s waterways).

Toilet

Toilet bombs

Pop one in the toilet for five minutes, scrub and flush away. Get them at Lil Bit.

Waste

Biodegradable trash bags

Hurrah. These do exist! Find them online at Biotuff and Flora & Fauna.

Biodegradable cotton buds. Photo: Shop Naturally

Biodegradable cotton buds. Photo: Shop Naturally

Comments (0)

06 July 2018

By portermathewsblog

popsugar.com.au

Image Source: A House in the Hills

If there are rules that you as a renter must follow, make it these 10 commandments. Because, while paying your rent on time is important, so too is making sure your place is personalised and stylish. Working within the boundaries of your landlord, it’s little things like a new light fixture that will make an impact without costing a lot of time or money. And, the best part about this entire list is that you’ll leave with your security deposit intact once it’s time to move up and on.

- Thou Shalt Add Storage

Let’s get real, custom cabinetry is not an option if you don’t own the place. Since rentals usually lack storage, add your own with affordable Ikea bookcases, simple shelves, or these organising solutions.

- Thou Shalt Change the Hardware

Rental hardware is basic . . . your style, not so much. Switching out cabinet pulls and bathroom hardware will make a huge difference. Just remember to keep the original pieces to swap back in before moving out.

- Thou Shalt Ditch Vertical Blinds

Image Source: Dana Miller for House*Tweaking

They are the ultimate decorating sin! To prevent your space from looking like a hospital room, take them down or hide them under curtains. Again, don’t toss — they’re essential if you want your security deposit back.

- Thou Shalt Line Cabinets

This might seem trivial and a bit annoying, but lining your cabinets is a must. Not only will it make your kitchen look clean, but also it will mask worn and grungy cabinets without having to paint. Adhesive liner works, but a softer grip liner is better because it’s easy to install; it will also prevent glassware from chipping.

- Thou Shalt Accessorise Like Crazy

It’s true, and that’s the only way you’re going to get a truly personal space. Go to town with throws, pillows, and accents that reflect your style.

- Thou Shalt Avoid Wallpaper

Well, in most cases. Sure it’s stylish, but in all honestly, wallpaper is really inconvenient to remove, especially if you won’t be in your place for long. If you love the patterned look, consider the removable wallpaper seen in this studio or these alternative wallpaper ideas.

- Thou Shalt Hang Art

Image Source: Love Grows Wild

No excuses — get your art on the walls! Patching up a tiny hole come move-out day is nothing compared to the impact it will make on your space. No need to create a full-blown gallery wall either. Try hanging one statement piece and resting photos on a mantel or shelf, similar to this home.

- Thou Shalt Invest in Rugs

Especially if your place has carpet! Rugs are an easy way to cover up that not-so-cute carpet and can be packed up with you come your next move. Rugs are also a necessity to keep noise down, especially in older apartments with wood floors.

- Thou Shalt Emphasise Lighting

Image Source: POPSUGAR Photography

This is another trick that many renters often overlook. Take it from HGTV stars Anthony Carrino and John Colaneri who suggest you use lighting to set the tone and make an impact in a rental. Get creative with floor and table lamps that can easily be moved from place to place.

- Thou Shalt Make the Most of Plants

No yard? No problem. Pots are a great way to achieve the bohemian jungalow look or even have your own urban garden. The best part is you won’t have to fret about leaving any of them behind.

Comments (0)

18 June 2018

By portermathewsblog

via therealestateconversation.com.au

Buying and selling property in WA has traditionally been by way of a conventional private treaty arrangement, however buyers and sellers are missing out on a more pure form of transaction, and that’s the auction.

Granted, auctions are becoming a more accepted selling method and the numbers of weekly auctions in WA has increased significantly over the past five years, but still lag a long way behind private treaty sales and the Eastern states. So why is that we’ve been slow to jump on the auction bandwagon?

Firstly, WA’s law for property transactions using the current “Offer & Acceptance” method protect both buyer and seller and in the majority of cases are easy to follow. The system works effectively for all parties to the transaction including the buyer, seller, settlement agent/conveyancer and banks. The downside of this system is that is can be time consuming and in many cases is conditional upon buyers obtaining finance, property inspections, having to sell their current home, etc.

More importantly, the system has a major flaw in it and that’s the asking price is disclosed and typically buyers knock the price down to where they feel comfortable – so it’s not good for sellers.

So why should we look to auctions? The auction system is the most pure form of selling and buying as there are no “secrets” surrounding price or selling terms; all terms are provided in the marketing campaign and the buyers set the price on where they see value. Selling by auction in most cases is quicker than private treaty. And the seller has three bites of the cherry; sell before auction day, on auction day or usually within 30 post auction day.

There are two main misconceptions surrounding auctions:

1. They cost too much. The cost of the auction is merely the auctioneer’s fee for calling the auction and working with the seller, buyer and agent to achieve the desired result. Typically, an auctioneers’ fee is in the vicinity of $700 to $1000. All other costs are associated with the marketing campaign to promote the property.

2. Auctions only “work in expensive areas”. That’s just a suburban myth. There’s many examples of properties below the current Perth median price of $510,000 selling at auction.

WA is one of only two states, the other being Tasmania, that don’t have a cooling off period in our property contracts. A cooling off period allows the buyer to “break” the Offer to Purchase usually between 2 to 5 business days after the offer has been signed. In other words, if the buyer changes their mind for whatever reason they can legally break the offer and walk away for a very small consideration to the seller, usually between 0.2% – 0.25% of the purchase price.

As WA doesn’t have cooling off provisions in our property contracts, this makes it far too easy for sellers and agents to default to Private Treaty transactions. If cooling off provisions were introduced to our property contracts, I’d predict a huge increase in the number of property auctions taking place in WA.

Finally, too few real estate agents embrace auctions and the auction process with vigor. They lack confidence and in some cases, the ability to explain the different marketing options available to sellers and automatically default to Private Treaty. This is a marketing injustice to sellers and the sooner we can demystify and legitimise the auction process for both buyers and sellers, the better.

Comments (0)

11 June 2018

By portermathewsblog

via therealestateconversation.com.au

Buying your first property is hard, so let’s make it easier for you.

Congratulations! You have decided to take the plunge, you have done some reading on what the various responsibilities when it comes to being a homeowner, you have spoken to the bank and have an idea of how much you are able to afford.

These steps take some time so we are here to encourage you to take the next step in home ownership. We know it’s a little bit nerve wrecking and a little bit scary, but we have compiled some advice from our in house experts to help you with this exciting time!

Looking for affordability without compromising on location

For many of us, your first home is not going to be your forever home. We recommend taking a holistic approach to purchasing property. Even if you are going to be living in that property, look at it as an investment as well.

For those first homebuyers who do not want to compromise on space, you may have to look further out depending on your budget or look for townhouses or terraces. If you are looking to keep more of your lifestyle, an inner city apartment may be the apt living situation for you.

What we emphasise is buying smart and seeing your home purchase as more than just a living situation but a step in growing your portfolio. You might want to ask yourself “How much rent will I get for this apartment?” or “What has been the capital growth in the area over the last few years?”.

We think asking these questions will not only give you peace of mind if you have to move out and rent or sell your property, but it is also how many people start their property portfolio. The first one does not have to be picture perfect, but it helps if it is a sound investment.

Location and amenities

The building, home or internal features are not the only things that you should consider when you buy. Are you in a desirable school catchment zone, are there amenities or transport facilities planned in your area or has a new shopping centre been planned?

Looking at the amenities and area around you is particularly important, as they are great financial health indicators that the area you are looking to buy in has infrastructure and amenity to attract people to live there.

Look on suburb out from your dream location

Looking for undervalued suburbs next to the pricier areas is always a something we recommend to our first home buyers – over time, population growth and gentrification will mean that there will be capital growth in your area.

It’s always good to also look at areas with employment growth as this will increase demand for homes in that area. Finally, do your research. It takes time to go through all the listings in the area you love and view the various prices they get sold for but it’s all worth it when you know you are on to a great purchase.

Comments (0)

06 June 2018

By portermathewsblog

via reiwa.com.au

The latest REIWA Curtin Buy-Rent Index for the March 2018 quarter has revealed it’s the best time to buy in Perth since 2013.

The latest REIWA Curtin Buy-Rent Index for the March 2018 quarter has revealed it’s the best time to buy in Perth since 2013.

The Index, released quarterly, assesses whether it’s better to buy or rent in Perth based on past and current trends in the economic and property market climate.

REIWA President Hayden Groves said the March 2018 quarter index showed the annual rate of house price growth required over 10 years to break even in the Buy-Rent Index had declined from 3.3 per cent to 3.1 per cent over the quarter, suggesting an improvement for prospective homebuyers weighing up the decision.

“To put that into perspective, Perth’s annual house price growth rate has been 5.9 per cent for the last 15 years. Based on the March 2018 quarter Index, house prices in Perth would only need to grow by more than 3.1 per cent annually for buying to be considered more financially beneficial than renting,” Mr Groves said.

“This improvement in buying conditions can be attributed to the Perth median house price softening by 1.9 per cent during the March quarter, while the median house rent price increased $5 to $360 per week. We also saw the 10 year average mortgage rate drop to 6.43 per cent, which means home owners are paying less on their mortgage repayments.

“This is the most affordable buying environment we’ve seen in Perth for some time, so if you’ve been weighing up whether to buy, now is the time to take advantage of favourable market conditions,” Mr Groves said.

Mr J-Han Ho, a Property Researcher and Senior Lecturer in the School of Economics and Finance at Curtin University, said the data indicated a continued improvement for the home buyer in the near future.

“Our analysis shows home buyers gaining an advantage, largely due to the low interest rates for home loans, home ownership costs continuing to be affordable and the median rents stabilising,” Mr Ho said.

View the March 2018 quarter Buy-Rent Index.

Comments (0)

28 May 2018

By portermathewsblog

reiwa.com.au

One of the most widely misunderstood elements of real estate is what condition a property should be in at settlement or possession.

One of the most widely misunderstood elements of real estate is what condition a property should be in at settlement or possession.

What does ‘buying as inspected’ really mean?

In short, a property is sold “as inspected”. If there was dust on a ceiling fan when you first inspected before contracting to buy then the fan can be dusty at settlement. The same goes for a dirty oven, a blown light globe or a squeaky laundry door. If it was dirty, blown or squeaky at inspection before purchase then so it should be at settlement.

Buyers will typically expect that the property is handed over to them spick n’ span and thankfully most house-proud sellers leave their homes in an appropriate condition when moving out, however legally there is no obligation for them to do so.

What should you expect at settlement?

If you’re buying a home, it’s smart to have a realistic expectation of what to expect at settlement.

Unless otherwise specified in the contract, the seller is under no obligation to have the property professionally cleaned for settlement and it is surprising how few buyers ask that such a condition be included.

The seller’s only obligation under the contract (Clause 6.1(b) 2 of the General Conditions) is to “…remove from the Property, before possession, all vehicles, rubbish and chattels, other than the Property Chattels.”

Many modern contracts to purchase include provision for essential plumbing, gas and electrical components to be working at settlement. Hence, if at settlement the toilet cistern leaks then the seller ought to make good because the contract says so.

It is trickier when, for example, a telephone jack doesn’t work at settlement. It is not strictly electrical but it is probably reasonable for a buyer to assume that it was functioning at inspection. This is partly because, caveat emptor (buyer beware) has all but disappeared according to some legal practitioners. The onus is probably on the seller to disclose (in this case) that the telephone jack didn’t work.

How to ensure you’re happy with the property at settlement

My view is that buyers need to take reasonable steps to ensure the property they have bought will be presented to them in a condition they are satisfied with.

This can be achieved by either contracting with the seller to guarantee it and/or being more thorough when inspecting the property in the first instance. Ask the agent if it’s ok to turn on taps, flush loos, flick switches, open and close doors, open the oven, turn on the dishwasher and so on before making an offer to purchase.

Buyers ought to have a realistic expectation of what to expect at settlement when buying an established home and acknowledge that opinions of presentation are subjective.

Speak to our market experts on 9475 9622 to discuss about your property concerns

Comments (0)

21 May 2018

By portermathewsblog

via reiwa.com.au

First home buyers are active in Perth’s property market, with data for the March 2018 quarter revealing an increase in sales for properties priced $500,000 and below.

First home buyers are active in Perth’s property market, with data for the March 2018 quarter revealing an increase in sales for properties priced $500,000 and below.

REIWA President Hayden Groves said after observing subdued first home buyer activity during the December 2017 quarter, it was pleasing to see the lower end of the market strengthen early in 2018.

“The final quarter of 2017 saw the composition of the Perth market shift. Last quarter there were significantly more sales in the higher priced end of the market and less in the first home buyer price range. It’s been a different story this quarter, with the balance of sales shifting back to the lower end of the market,” Mr Groves said.

Median house and unit price

Perth’s preliminary median house price is $510,000 for the March 2018 quarter.

Mr Groves said once all sales settle, this figure was expected to increase to $517,000, which would put the March 2018 quarter median marginally lower (by 0.6 per cent) than the December 2017 quarter.

“Although Perth’s median house price experienced a minor adjustment during the March 2018 quarter, the median house price is up 0.4 per cent when compared to the same time last year, which shows prices are stable,” Mr Groves said.

Perth’s preliminary median unit price is $401,000 for the March 2018 quarter.

“This is expected to lift to $410,000 once all sales settle, which would put it equal with the December quarter median.

“These results are in line with REIWA’s 2018 forecast, which expects stable conditions throughout the remainder of this year, with moderate price growth during the next 12 months,” Mr Groves said.

Sales activity

Preliminary Landgate data shows there were 5,865 dwelling sales during the March 2018 quarter.

“We expect around 6,603 sales for the quarter overall, which is marginally lower than volumes recorded during the December quarter,” Mr Groves said.

There was a 5.7 per cent increase in house sales in the sub-$500,000 price range during the March 2018 quarter.

“Increased activity in the lower end of the market is usually a sign first home buyers are active. We are fortunate the dream of home ownership is more attainable for West Australians than it is on the east coast. After seeing activity drop off last quarter, it’s good to see first home buyers are increasing their presence in the market,” Mr Groves said.

Listings for sale

There were 14,413 properties for sale in Perth at the end of the March 2018 quarter.

Mr Groves said listings had increased 10.2 per cent over the quarter, but were down 2.9 per cent when compared to the March 2017 quarter.

“While it is pleasing listings have declined on an annual basis, the increase over the quarter is not cause for alarm. With overall sentiment in WA improving and all signs indicating the market has begun to turn, sellers are feeling more confident than they have been and therefore more inclined to put their property up for sale.

“We’ve also seen a sharp decline in rental listings over the past year which has had a flow-on effect to the established market. With some investors choosing to sell their rental property instead of lease it, this has contributed to the rise in the number of properties for sale in Perth,” Mr Groves said.

Average selling days

It took 67 days on average to sell a house in Perth during the March 2018 quarter.

Mr Groves said although average selling days increased over the quarter, it was still two days quicker to sell than it was during the March 2017 quarter.

“With more listings on the market, buyers now have more choice, which has had an impact on the time it takes to sell. It’s very encouraging though, that on an annual basis, we’re seeing average selling days decrease,” Mr Groves said.

Comments (0)